The Role of Alternative Data in Credit Scoring

Traditional credit scoring models often exclude millions of people due to limited financial history. Alternative data is transforming credit assessment by enabling lenders to make faster, fairer, and more inclusive credit decisions. At Spinmobile, we leverage alternative data to unlock financial access for underserved individuals and businesses.

Spincrunch

Access to credit remains a challenge for many individuals and small businesses, especially in emerging markets. Traditional credit scoring models rely heavily on bank statements, collateral, and formal credit histories—criteria that exclude a large portion of the population.

Alternative data is changing this narrative. By using non-traditional data sources, lenders can gain deeper insights into borrower behavior and creditworthiness. At Spinmobile, alternative data plays a central role in building smarter, more inclusive credit scoring solutions.

What Is Alternative Data in Credit Scoring?

Alternative data refers to financial and behavioral information that falls outside traditional credit bureau records. This data provides additional context about a borrower’s financial habits, stability, and reliability.

Common examples include:

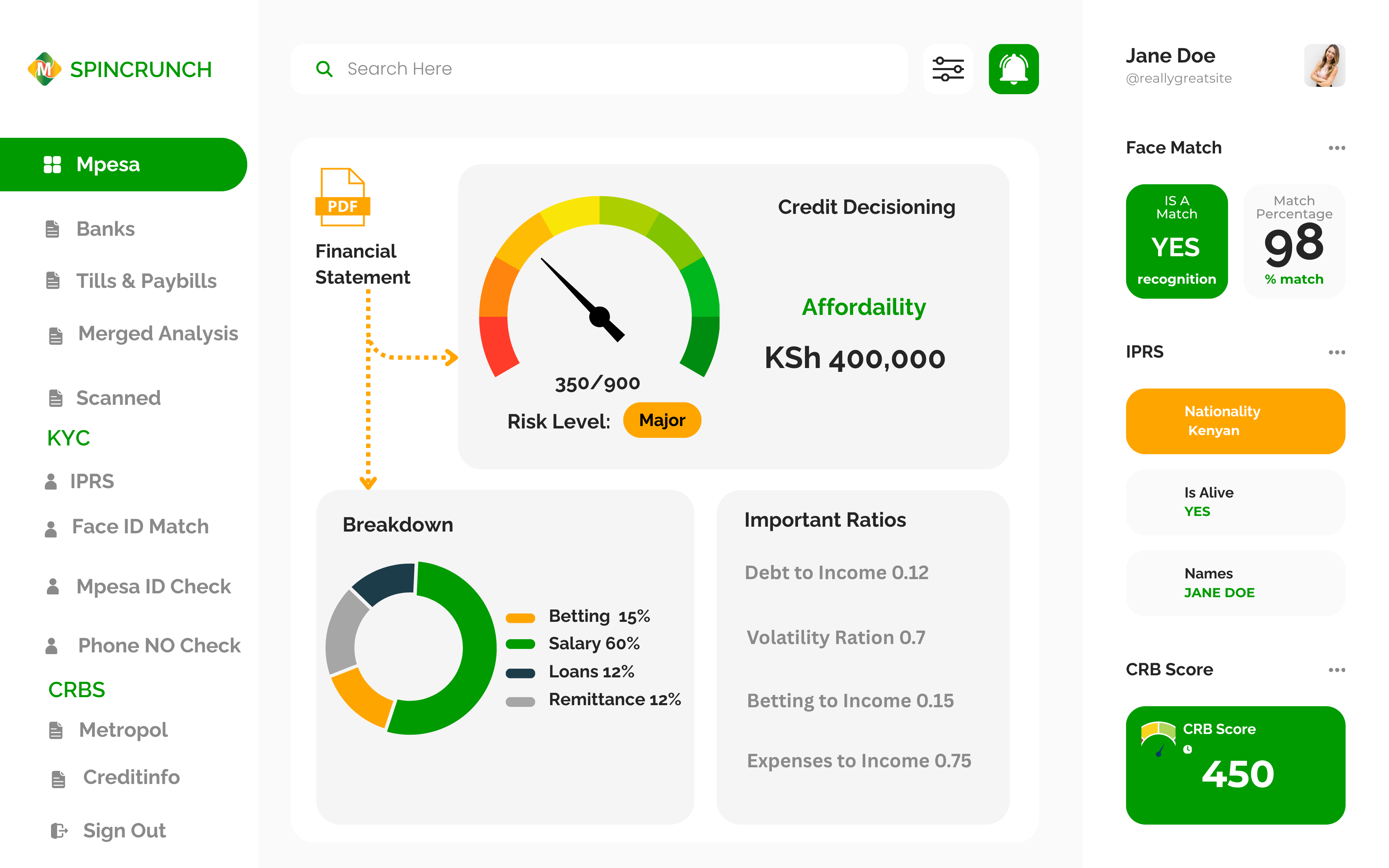

Mobile money transactions (e.g., M-Pesa activity)

Utility and rent payment history

Transaction descriptions and cash flow patterns

Business sales records and digital receipts

API-based data from trusted third-party providers

When analyzed correctly, this data can strongly correlate with repayment behavior.

Why Traditional Credit Scoring Falls Short

Conventional credit scoring models were designed for economies with high banking penetration. In reality:

Many individuals have no formal credit history

SMEs operate informally with limited documentation

Financial behavior is increasingly digital, not bank-based

As a result, otherwise creditworthy borrowers are often rejected or misclassified.

How Alternative Data Improves Credit Decisions

Alternative data enhances credit scoring in several key ways:

1. Financial Inclusion Borrowers with no credit bureau history can now be assessed fairly using real transaction data.

2. Better Risk Assessment Cash flow trends, income consistency, and spending behavior provide more accurate risk signals than static credit scores.

3. Faster Credit Decisions Automated data ingestion and analysis reduce turnaround time from days to minutes.

4. Dynamic Scoring Scores can evolve as new data is received, allowing lenders to adjust limits and pricing in real time.

Spinmobile’s Approach to Alternative Data

At Spinmobile, we integrate alternative data directly into our credit scoring engines. Our approach focuses on:

Transaction-level analysis from bank and mobile money statements

Machine learning models trained on real financial behavior

Secure API integrations with trusted data providers

Explainable scoring outputs for compliance and transparency

By analyzing patterns such as income frequency, expense categories, and repayment behavior, we generate actionable insights that lenders can trust.

Ensuring Data Privacy and Trust

The use of alternative data comes with responsibility. Spinmobile prioritizes:

User consent and data minimization

Secure data storage and encryption

Compliance with data protection regulations

Transparent scoring logic

Trust is essential for sustainable credit ecosystems.

The Future of Credit Scoring

As financial behavior continues to digitize, alternative data will become the standard—not the exception. Credit scoring will shift from rigid rules to intelligent, adaptive systems that reflect real-world financial lives.

Spinmobile is committed to driving this transformation by building technology that expands access to credit while maintaining accuracy, fairness, and trust.

Conclusion

Alternative data is redefining how creditworthiness is measured. By moving beyond traditional metrics, lenders can serve more people, reduce risk, and grow responsibly.

At Spinmobile, we believe inclusive credit starts with better data—and smarter ways to use it

More

Credit Scoring

One platform everything in credit scoring

Score

Based on credit history

2 images in gallery